Several studies have shown investors can feel overwhelmed by overly large investment menus. Large menus have been shown to decrease participation rates in retirement plans as participants weight their options1. But how big is too big when it comes to fund lineups?

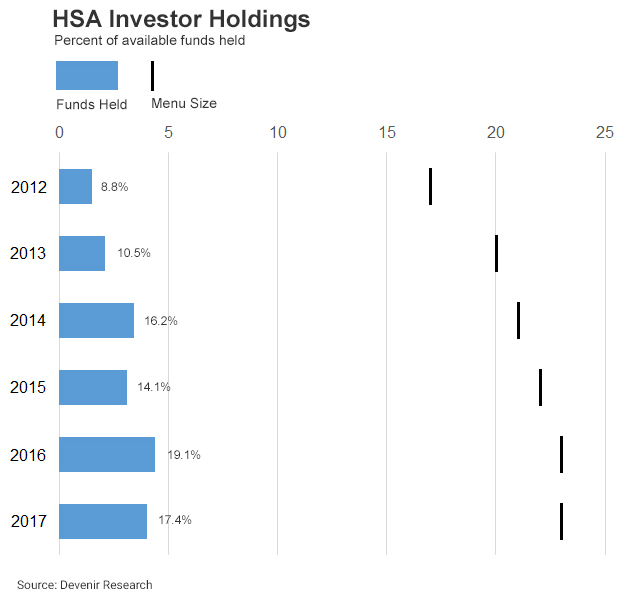

The relationship between menu size and the number of funds held by investors has generally been positive in the HSA market. Fund line-ups have expanded over time, and the average number of funds held by HSA investors has more than doubled, from 1.5 funds in 2012 to 4 funds in 2017, suggesting that investors will hold more funds when more funds are available.

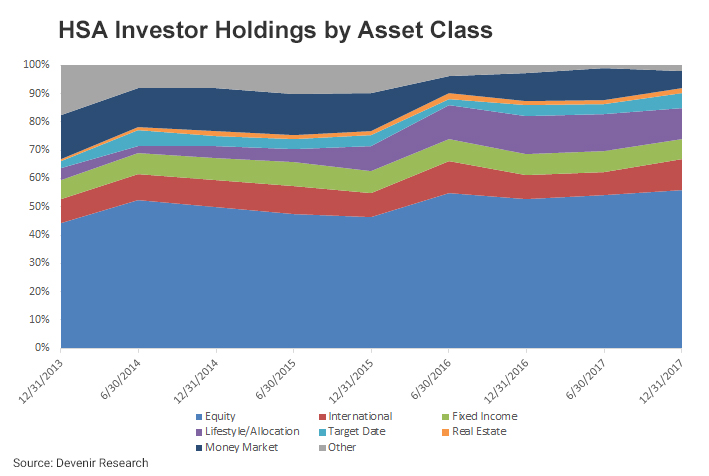

As the average number of holdings has increased however, investor asset class preferences have remained relatively consistent over time.

We have found that the proportion of equity funds offered in an HSA menu relative to bond or other funds can impact investor allocations as well. Research in the retirement plan space has also shown this impact2. Offering multiple funds within an asset class gives investors more choice, but too many options can cause inaction on the part of investors. Large fund line-ups may also be less effective in achieving the economies of scale required to reduce plan costs through share class enhancements. This is due to the reduced ability to meet minimum asset thresholds as plan assets are spread out across a larger number of funds. These are all considerations that can impact the number of funds to include in a menu, and the menu layout of asset classes offered.

Despite the potential pitfalls of adding too many options, there are benefits to having a larger than average fund list as well. With more room on the menu, it becomes more practical to add asset classes or fund strategies that may be favorable for certain market conditions or demanded by experienced investors. However, it may be helpful to add decision support tools and resources to help less familiar investors sort through a sizable offering.

Stay tuned to the Devenir blog for ongoing updates and insights into the HSA marketplace!

End Notes

1 Iyengar, Huberman, and Jiang, “How much choice is too much: determinants of individual contributions in 401(k) retirement plans,” in O.S. Mitchell and S. Utkus, Editors, Pension Design and Structure: New Lessons from Behavioral Finance, Oxford University Press, Oxford, pp. 83-95, 2004

2 ”Offering vs. Choice in Retirement Plans: A Cross Sectional Analysis of Investment Menus with Traditional and Life-Cycle Mutual Funds” Kam, McDonald, Richardson, and Rietz. September 2016. https://www.icpmnetwork.com/

Investments are not FDIC Insured and may lose value. The information above is intended to be used for educational purposes only and is not to be construed as investment or tax advice, or as tailored to any specific investor. Consult a financial advisor or tax professional for more information. This information may be affected by the laws of particular states and there is no guarantee this information will be consistent across all states. Alabama, California, and New Jersey may impose taxes on HSA contributions, earnings, and dividends. Additionally, New Hampshire may impose taxes on HSA contributions. Data used may be estimates and may not reflect actual observed data.